The best bank account for a small business in Illinois depends on how your business operates. There is no single answer for every business type. For owners who want $0 monthly fees, high-yield savings, and built-in accounting and tax tools, Lili is the strongest digital-first pick. For frequent cash deposits and in-person service, Chase and BMO have the deepest Illinois branch networks. For local relationship banking, Wintrust is the largest Illinois-headquartered bank. For SBA loans, Huntington and Wells Fargo lead. This guide compares them on what actually moves money: fees, APY, branch access, cash handling, lending, and the tools you use daily.

Illinois is home to roughly 1.2 million small businesses, more than 99% of the state’s employers, spanning Chicago professional services, downstate manufacturing and agriculture, and logistics along the rail and interstate corridors. It is also a high-cost tax state: a flat 4.95% individual income tax, a 9.5% combined corporate rate (third-highest in the nation), and Chicago sales tax at 10.25%. That makes controlling banking costs matter more here than in low-tax states, because your margins are already tighter.

Best bank Accounts for small business in Illinois: quick comparison

| Bank | Best for | Monthly fee | IL branches | Cash deposits | Savings interest |

|---|---|---|---|---|---|

| Lili | Digital-first SMBs wanting $0 fees + finance tools | $0 (Core plan) | None (online) | Limited, via retail network (fees apply) | 2.25% APY up to $500K; 4.00% APY on $500K-$1M |

| Chase | In-person banking and cash-heavy businesses | $15, waivable with $2,000 balance | 250+ | Yes, up to $5,000/mo free | Low base rate |

| BMO | Chicago full-service and cash management | Waivable with min. balance | Strong Chicago-area network | Yes, branch and ATM | Low base rate |

| Wintrust | Local relationship banking (largest IL-HQ bank) | No fee under 75 transactions/mo | ~170 community locations | Yes, branch and ATM | Varies by account |

| Huntington | SBA loans and lending relationships | Waivable with min. balance | Chicago-area branches | Yes, branch and ATM | Low base rate |

| Alliant Credit Union | Low fees, high-yield, member-owned | Low to none | Online-first (Chicago-based) | Limited (online model) | Higher member rates |

Lili is a financial technology company, not a bank. Banking services are provided by Sunrise Banks, N.A., Member FDIC. Rates and features are current as of 2026 and can change – verify before opening.

Lili: best for digital-first Illinois businesses

Lili is an award-winning online business banking platform built for growth-ready small businesses, including Illinois owners who run their operations online. Advanced business banking comes with built-in financial tools for accounting and taxes, so you’re not paying for branch overhead you never use. The free Core plan is designed for businesses managing real volume and complexity, from day one through higher-revenue, multi-employee stages.

What stands out:

- No monthly fee on the Core plan, no minimum balance, no overdraft fees, and no fees at MoneyPass ATMs. In a high-tax state, keeping fixed costs near zero directly protects thin margins.

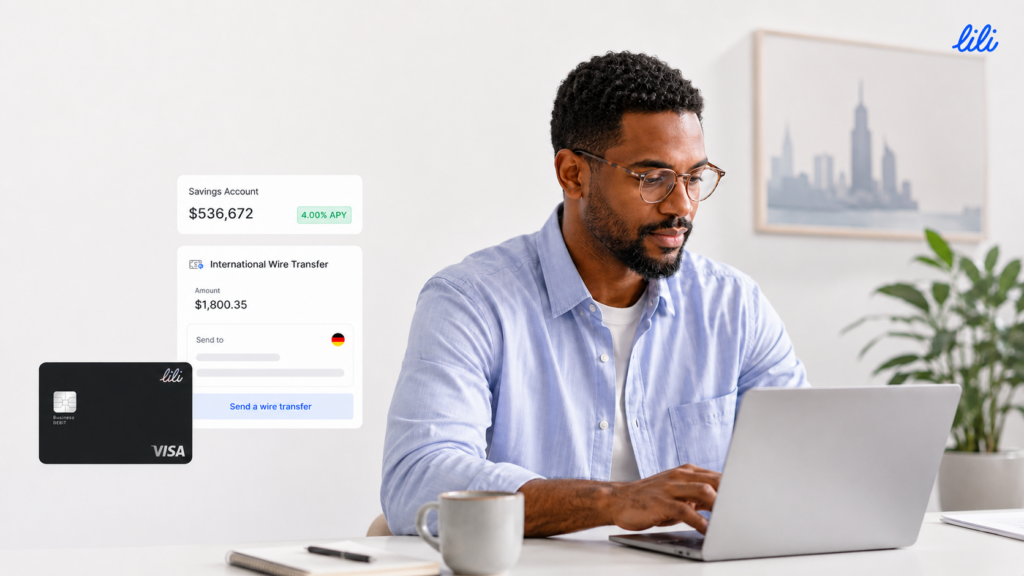

- High-yield business savings: 2.25% APY on balances up to $500,000 and 4.00% APY on the portion from $500,000 to $1,000,000. Savings is now available on every plan, including free Core, with no lockups.

- FDIC insurance up to $3 million through Lili’s sweep network of program banks. The standard FDIC limit is $250,000 per depositor per bank; Lili reaches higher coverage by spreading deposits across partner banks via Sunrise Banks, N.A. Useful for businesses holding payroll or working-capital reserves above the standard limit.

- Payments built for volume: Express ACH, expedited check deposits, and domestic and international wires (international wires for legal entities such as LLCs and corporations).

- Built-in finance tools: invoicing, expense tracking, tax prep, and reporting on paid plans, plus 50+ integrations with QuickBooks, Xero, Stripe, Shopify, Gusto, and Square.

- Team and accountant access, plus credit-building through BusinessBuild, flexible financing solutions and seven-day live support.

Plans: Core ($0), Pro ($15/mo), Smart ($35/mo), and Premium ($55/mo). The paid tiers add tax savings buckets, advanced reporting, and accounting software. Note that some older roundups still list Lili’s Pro plan at $9/month and savings at 4.15% APY; those figures are outdated, so confirm current pricing before you cite it.

The honest limitation: Lili is not built for cash. There are no fee-free cash deposits, and cash goes through a retail partner network with fees and limits. If your Illinois business takes meaningful cash – a Chicago retail shop, a cash-paid trade – a bank with branch and ATM deposits will serve you better. For service, online, ecommerce, and B2B businesses paid by ACH, card, or wire, that limitation rarely matters.

Fast payments, up to 4.00% Annual Percentage Yield (APY), and up to $3M in FDIC insurance

Chase: best for in-person banking and cash deposits

Chase has more than 250 branches across Illinois, with a dense Chicago-area presence, and one of the strongest digital platforms among national banks. Chase Business Complete Banking includes built-in card processing through QuickAccept, so retail and restaurant owners can take payments without a separate merchant account. The account carries a $15 monthly fee, waivable with a $2,000 minimum daily balance, and includes up to $5,000 in cash deposits per month before fees apply. New-customer bonuses are common. The trade-off is small-business lending that can be less flexible than a community bank’s.

BMO: best for Chicago full-service banking

BMO is headquartered in Chicago and has one of the strongest metro-area networks in the state, which makes it a practical full-service option for businesses that want branch access plus treasury and cash management under one roof. It offers fee waivers with minimum balances and a broad lending menu. If your operations are Chicago-centered and you value an in-person banking relationship, BMO is worth a look alongside Chase.

Wintrust: best for local relationship banking

Wintrust is the largest Illinois-headquartered bank, operating around 170 community-bank locations under local brand names across the state. Its model is relationship banking: a designated business banker, local decision-making, and no-fee business checking for accounts under roughly 75 transactions per month. For Illinois owners who want a banker who knows their market and can move on a loan quickly, Wintrust is a strong regional choice.

Huntington: best for SBA loans in Illinois

Huntington is a leading SBA lender with Chicago-area branches and a full slate of SBA 7(a), 504, and Express programs, which makes it worth it to consider if borrowing is on your roadmap. Wells Fargo is also one of the country’s top SBA 7(a) lenders, though its Illinois branch footprint is thin, so it works best if you are comfortable handling the lending relationship without frequent branch visits. Weigh the monthly fee against the value of the lending relationship.

Alliant Credit Union: best low-fee, high-yield option

Alliant is a Chicago-based, digitally focused credit union available nationwide, known for low fees and higher-than-average yields. As a member-owned institution, it typically beats traditional banks on rate and cost. The trade-offs are membership requirements and an online-first model that, like a fintech, is not ideal for frequent cash deposits. It suits Illinois owners who want credit union economics without giving up a modern app.

Online vs traditional vs credit union: which fits your Illinois business?

Online platforms (Lili, and other fintechs) come out ahead on cost and tools. No branches means lower overhead, which translates to $0 or low monthly fees, higher savings yields, and software that connects to your accounting stack. Best for service providers, ecommerce, startups, and any business paid digitally.

Traditional national and regional banks (Chase, BMO, Wintrust, Huntington) are strong on cash handling, in-person service, and broad lending, including SBA loans. Best for cash-heavy businesses and owners who want a local banker.

Credit unions (Alliant) win on low fees and higher yields. Best for owners who prioritize rate and cost over branch access.

Many Illinois businesses run a hybrid setup: a digital platform like Lili for everyday operations, savings, and bookkeeping, plus a traditional account for cash deposits or a specific lending relationship.

How to choose the best bank for your Illinois business

Weigh these in order of how much they cost you:

- Fees. A “no monthly fee” headline doesn’t tell the full story. Check wire fees, ACH fees, cash deposit fees, and out-of-network ATM fees. Check wire fees, ACH fees, cash deposit fees, and out-of-network ATM fees. Illinois already taxes businesses heavily – a 9.5% combined corporate rate and high property taxes – so trimming banking fees is one of the few costs fully within your control.

- Cash handling. If you take cash, prioritize branch and ATM deposits. If you don’t, you can trade that away for lower fees and better tools.

- APY. Idle operating cash should earn. A high-yield savings account paying 2.50% or more beats the near-zero rates on most traditional business savings.

- Tools and integrations. Invoicing, accounting, and tax features that sync with your account save hours every month, which matters given Illinois’s replacement-tax and franchise-tax filing complexity.

- FDIC coverage. Confirm where deposits sit and how much is insured. Coverage above $250,000 requires a sweep or multi-bank structure.

- Lending and growth. If you expect to borrow, prioritize a strong SBA lender or a relationship bank with local decision-making.

What you need to open a business bank account in Illinois

Have these ready before you apply:

- Your IRS-issued EIN

- Formation documents filed with the Illinois Secretary of State (Articles of Organization or Incorporation)

- A government-issued photo ID for anyone with operating control and any owner holding 25% or more

- Your business license, if applicable, plus any Chicago or county licensing your activity requires

Online platforms like Lili let you open an account from your phone with no branch visit, often with near-instant approval for sole proprietors. National banks allow online opening too, and Illinois credit unions like Alliant typically offer online applications as well.

Common mistakes Illinois business owners make

- Choosing on brand familiarity instead of fit. Your personal bank is not automatically your best business bank.

- Ignoring savings yield. Leaving reserves in a 0.01% account costs real money, especially when every other cost in Illinois is climbing.

- Picking a fee-free online account, then realizing you take cash. Map your payment mix first.

- Overlooking FDIC structure. Assuming every dollar is covered without checking the per-bank limit.

- Mixing personal and business funds. A dedicated business account protects your liability shield and simplifies the replacement-tax and franchise-tax filings Illinois requires.

How Lili helps Illinois small businesses

For Illinois owners who do most of their banking online, Lili removes the usual trade-off between low cost and real capability. The free Core plan gives you a full business checking account with no monthly fee, expedited payments, and FDIC coverage up to $3 million through its sweep network – protection that used to require juggling multiple bank accounts. Your operating cash earns 2.50% APY up to $500,000 with no minimum and no lockups, and savings is included even on the free plan. In a state where taxes and property costs eat into margins, keeping banking fees near zero is a rare lever you fully control.

Because Lili connects banking, invoicing, expense tracking, and tax prep in one place, a Chicago agency or a downstate ecommerce seller can close the books without exporting data between five tools – useful when Illinois filing includes replacement tax and franchise tax on top of federal. Team and accountant access, plus integrations with QuickBooks, Xero, Stripe, and Shopify, keep everything in sync as you scale. If your business runs on digital payments rather than cash, Lili covers the day-to-day and gives your reserves a place to grow.

FAQ

What is the best bank for small business in Illinois?

It depends on how your business operates. Lili is the best fit for digital-first businesses wanting $0 fees and built-in finance tools; Chase and BMO are best for cash deposits and in-person banking; Wintrust is the largest Illinois-headquartered bank for local relationship banking; Huntington and Wells Fargo lead for SBA loans.

Can I open a business bank account in Illinois online?

Yes. Lili, Chase, Bank of America, and Bluevine all allow online opening for Illinois businesses. Lili is fully online with no branch visit. Illinois credit unions like Alliant also typically offer online applications.

What do I need to open an Illinois business bank account?

Your EIN, formation documents filed with the Illinois Secretary of State, a government-issued photo ID for anyone with control or 25%+ ownership, and a business license if your activity or city requires one.

How do Illinois business taxes affect banking decisions?

Illinois has a flat 4.95% individual income tax and a 9.5% combined corporate rate (7% income tax plus a 2.5% personal property replacement tax) for C-corporations, third-highest in the nation. Pass-throughs pay a 1.5% replacement tax. Because the tax burden is high, minimizing banking fees and earning yield on reserves has an outsized impact on what you keep.

Is a fintech account like Lili FDIC insured?

Yes. Lili is a financial technology company, not a bank, and banking services are provided by Sunrise Banks, N.A., Member FDIC. Deposits are insured up to $3 million through a sweep network of partner banks, above the standard $250,000 per-bank limit.

Which bank is best for a cash-heavy Illinois business?

A traditional bank with branch and ATM access, such as Chase, BMO, or Wintrust. Online platforms like Lili and online-first credit unions like Alliant are not built for frequent cash deposits.

What APY can an Illinois small business earn on savings?

With Lili, business savings earns 2.25% APY on balances up to $500,000 and 4.00% APY on the portion from $500,000 to $1,000,000, with no minimum balance. Most traditional Illinois banks pay far less on business savings, though member-owned Alliant Credit Union is competitive.