Here are six of the best online bank accounts for e-commerce businesses—all with no monthly maintenance fees and above-average TrustPilot ratings.

As an e-commerce founder, you need a business bank account that integrates smoothly with your tech stack, supports fast payouts, and keeps operating costs low. But with so many options, it can be hard to decide which one to choose. You’ll encounter accounts from traditional banks and modern fintechs—each with different fees, features, and benefits. So, how can you narrow down your options and find a good fit? We’ve done some of the hard work for you. Here’s a guide on what to look for as you compare accounts—along with our picks for the six best online bank accounts for e-commerce businesses in 2026.

Who provides bank accounts for e-commerce businesses?

As you start shopping for a business bank account, you’ll likely find accounts from three main types of financial institutions:

- Traditional banks: Traditional banks are long-standing financial institutions, such as Wells Fargo and Bank of America, with large networks of brick-and-mortar branches. These institutions tend to be best for founders who prefer in-person banking and are willing to pay more for it.

- Fintech companies: Fintech companies, such as Lili and Mercury, partner with banks to offer full-service online bank accounts to business owners. These providers tend to offer lower-cost, tech-forward solutions, but lack the in-person customer support of traditional banks.

- Global payment platforms: Global payment platforms, such as PayPal and Wise, can hold balances and facilitate money transfers but don’t offer full-service bank accounts. They typically supplement a founder’s bank account rather than replacing it.

When comparing the three options, online business bank accounts are often the best fit for e-commerce founders who are tech-savvy, comfortable managing their finances fully online, and looking for the best value. For those who don’t want to give up their local branch and in-person service, a traditional bank will likely be better. However, the decision doesn’t end with choosing a type of bank account provider. Next, you’ll need to decide which business bank account best suits your needs from that type of provider.

What to look for in an online business bank account for your e-commerce company

If you decide to move ahead with an online business bank account, you’ll find no shortage of fintechs with offerings. As you compare them, these ten factors tend to be the most important for e-commerce founders:

- Adequate FDIC insurance: Ensure your deposits are protected. Standard FDIC insurance covers up to $250,000 per depositor, per insured bank account, but a growing number of fintech platforms are offering higher limits through partner bank networks.

- Low fees: Look for accounts with minimal fees, especially on the services you’ll use the most.

- Suitable limits: Check a provider’s limits for various transaction types, such as incoming ACH transfers, outgoing ACH transfers, debit card purchases, and ATM withdrawals. Ensure they align with your typical business needs.

- Financing: Direct access to business credit through your bank can help your company access capital more easily. Look for term loans, lines of credit, and credit cards.

- Annual Percentage Yields (APY): Some bank account providers pay interest on your balance. Look for a competitive APY that will help you earn passive returns.

- Payment processor compatibility: Check if a bank account integrates smoothly with your e-commerce payment processors and supports fast payouts.

- Financial software and automation: Consider if the account comes with software to automate and streamline your financial operations (e.g., accounting, taxes, cash flow monitoring, etc.).

- Other integrations and apps: Look for direct integrations with the apps you use, such as QuickBooks, WooCommerce, and Xero.

- Global payment capabilities: If you operate internationally, look for international wires, low-cost currency conversions, and no foreign transaction fees.

- Quality customer service: Check customer support channels and hours, along with reviews from past customers. Reliable, quality customer service will be critical when issues arise.

As you prepare to research bank accounts, it can help to create a spreadsheet with the factors that are most important to you (see the example below). From there, you can compare the accounts side by side at a glance.

Best online bank accounts for e-commerce businesses

Now, for our top picks. If you’re not sure where to start your search for an online business bank account, here are six of the best options we recommend for e-commerce businesses in 2026.

Lili’s Core Plan

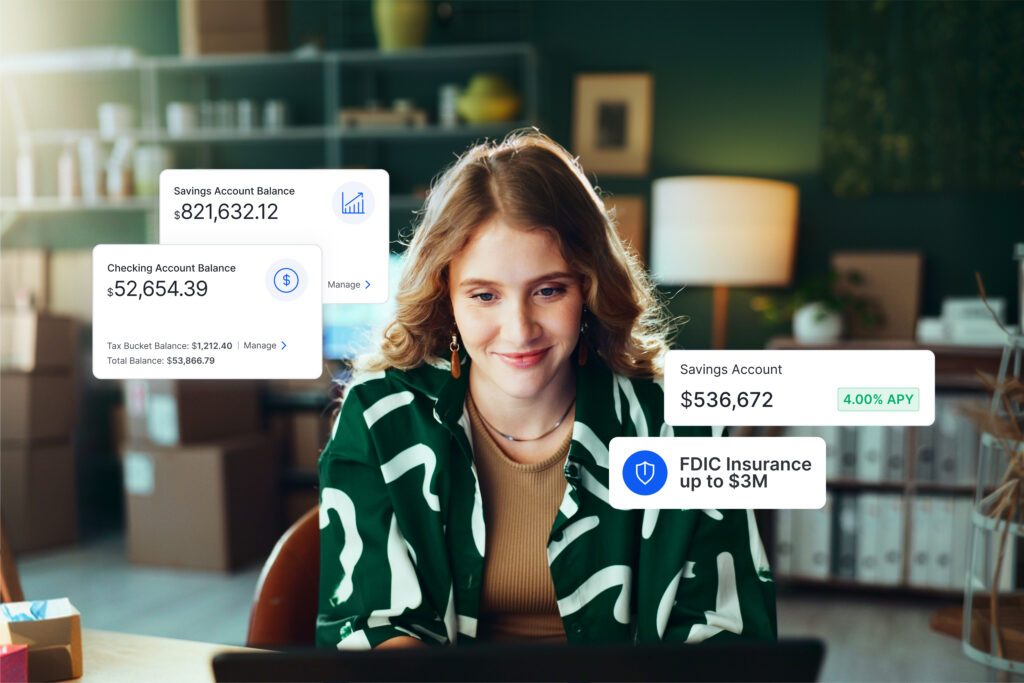

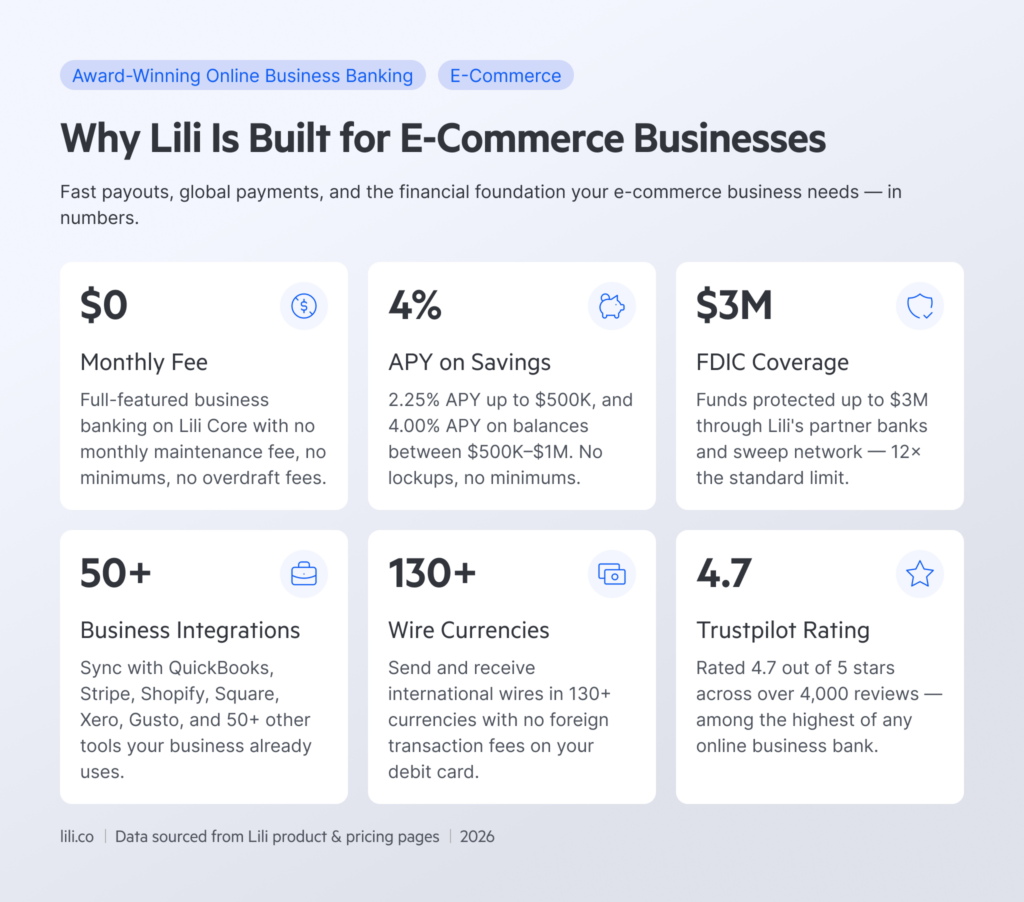

Lili’s Core is a no-monthly-service-fee plan, which can be a great fit for e-commerce founders—especially those who do business globally. The account offers fast domestic payments, international wires in over 130 currencies, no foreign transaction fees, expedited check deposits, and fee-free withdrawals at MoneyPass ATMs. Additionally, it can sync with over 50 business tools, connect you with financing opportunities, and offer up to $3 million in FDIC insurance. As for interest earnings, Lili offers one of the highest yields—2.25% APY on balances up to $500,000, and 4.00% APY on balances from $500,001 to $1,000,000.

NorthOne’s Standard Plan

NorthOne’s Standard plan includes an online business checking account with no monthly fee, standard and low-cost express ACH transfers, and instant deposits from third-party platforms like Stripe and Square. That last feature means very little waiting for funds to transfer from your payment processors to your bank account. NorthOne also offers fee-free ATM withdrawals at Allpoint ATMs, lending options, automated reporting, and budgeting and bill payment tools. On the downside, the company doesn’t support international wire transfers and only offers up to $250,000 in FDIC insurance.

Novo’s Only Plan

Novo is one of the few companies that offers just one plan. However, it has no monthly fee and is worth considering due to a solid lineup of features, including free ACH and low-cost express ACH transfers, financing options, and bookkeeping and budgeting tools. Further, it enables a lineup of direct integrations, features exclusive partner discounts, and supports international wire transfers through a Wise integration. But there are a few drawbacks. Novo doesn’t have a fee-free ATM network, and FDIC insurance is limited to $250,000. Additionally, the company doesn’t pay interest on balances and only allows cash deposits via money orders—which is rare amongst competitors.

Found’s Found Plan

Found offers three plans with business bank accounts. The base plan has no monthly fee and offers up to 10 subaccounts called Pockets, team debit cards with spending controls, and payment integrations. It also includes software to help with bookkeeping and taxes, unlimited invoicing, and both standard and low-cost express ACH transfers. However, Found doesn’t pay interest on your balance, limits FDIC insurance to $250,000, and doesn’t support international wires.

Bluevine’s Standard Plan

Bluevine offers a Standard plan with no monthly fee that includes up to $3 million in FDIC insurance, a 1.3% APY on balances up to $250,000, standard and low-cost same-day ACH payments, and support for international wires. You can also earn 4% cash back on business purchases with over 50,000 merchants, apply for Bluevine financing, and enjoy fee-free access to MoneyPass ATMs. On the downside, the APY isn’t guaranteed. To get it, you must spend $500 per month with your Bluevine debit card or receive $2,500 in customer payments into your Bluevine bank account.

Relay’s Starter Plan

Relay offers a Starter plan with no monthly fee, designed for solopreneurs. The account offers standard and low-cost express ACH transfers, international wires, fee-free withdrawals at AllPoint ATMs, and accounting integrations. Further, it pays 0.91% APY on savings account balances, allows up to 20 checking accounts, and offers up to $3 million in FDIC insurance. As for lending, the company has a Relay Capital program in beta, but its not yet widely available.

| Bank Name | FDIC Insurance Cap | International Wires | APY Cap on Free Account | Foreign Transaction Fee (Debit Card) | TrustPilot Rating/Review Count |

| Lili | $3,000,000 | Yes | 4.00% | $0 | 4.7 stars; 4,080 reviews |

| NorthOne | $250,000 | No | 2.50% | $0 | 4.1 stars; 270 reviews |

| Novo | $250,000 | Yes | No | .8 to 1% | 4.0 stars; 4,498 reviews |

| Found | $250,000 | No | No | Not specified | 4.6 stars; 1,243 reviews |

| Bluevine | $3,000,000 | Yes | 1.30% | Not specified | 4.6 stars; 10,124 reviews |

| Relay | $3,000,000 | Yes | 0.91% | 1-2% fee added by Visa | 4.3 stars; 3,055 reviews |

Methodology for choosing the best business bank accounts for e-commerce businesses

The Lili team selected the best business bank accounts for e-commerce businesses after evaluating a lineup of account providers according to a selection of key features. We considered FDIC insurance limits, account fees, transaction limits, support for international wire transfers, direct integration options, expedited domestic payments, interest yields, TrustPilot ratings and reviews, ATM networks, and more. The top picks each offer a business bank account plan with no monthly fee, have earned a TrustPilot rating above 4.0 stars, and have a competitive overall online offering with features that support e-commerce businesses.

Essential requirements for opening an e-commerce business bank account

Once you decide on a bank account and are ready to move forward, the provider will typically request the following:

- Information to verify the owners: A government-issued ID for each owner, along with personal identifying information, such as your name, phone number, email address, Social Security number, birth date, and personal address.

- EIN: Businesses must have an EIN and must submit their IRS EIN letter.

- Documentation to verify the business: To verify the business is a legal entity, you’ll often need to provide formation documents, such as the Articles of Organization, Articles of Incorporation, Operating Agreement, and/or Partnership Agreement.

- Business physical address: Account providers generally require proof of the business’s physical address, such as a utility bill, government-issued ID, signed lease agreement, or tax documents from the most recent year.

Having these documents ready ahead of time can help to streamline the application process and avoid delays.

Find the right business bank account for your e-commerce company

The right business bank account for your e-commerce company is the one that best fits your business needs in terms of features, user experience, and cost. Consider the features and services you need and want most from an account, such as payment integrations, low fees, and a competitive APY. From there, review the fee schedules, deposit agreements, and reviews of a handful of reputable business bank account providers to find the best fit. If you’re not sure where to start, consider the six accounts listed above.

E-commerce business bank account FAQs

Find answers to frequently asked questions about business bank accounts for e-commerce businesses.