The best online bank account for most small businesses is Lili, with a $0 monthly fee, cash deposits at 90,000+ retail locations, up to $3M in FDIC insurance, and up to 4.00% APY on savings. Mercury is the top pick for tech startups and low-cost money transfers, and NorthOne pays the highest APY on balances under $250,000. The right choice depends on the needs of your business and how you move money, so we’ve evaluated a lineup of leading online small business banking options across 17 key feature categories, including deposit options, ATM networks, fees, FDIC insurance, and more. Read on to find our five top picks along with a detailed comparison table. From there, you can use the quick decision guide at the bottom to hone in on the best fit for your small business.

Quick Answer – Top 5 Picks (Shortlist)

Which bank is the best for small business owners in 2026? Here are our top five picks!

Best overall – Lili

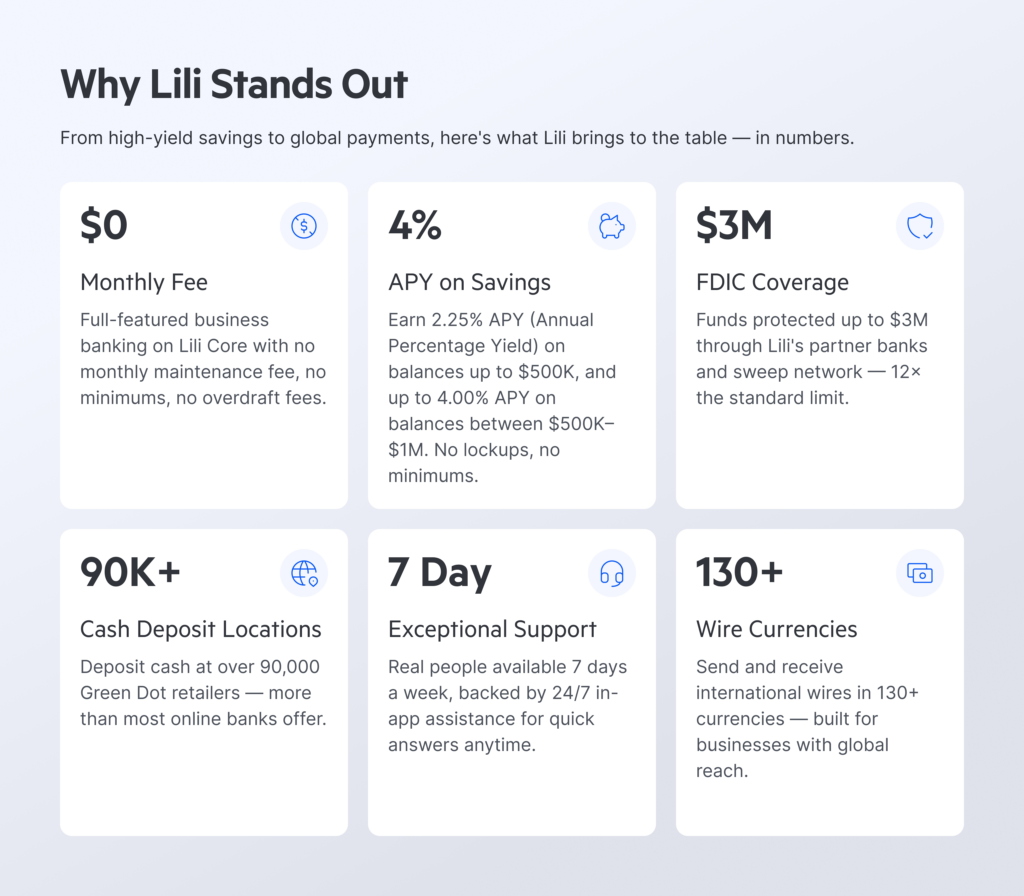

Lili offers an advanced online bank account that is competitive across the board. Highlights include cash deposits at over 90,000 retail locations, $0 monthly fee, free ATM access at over 40,000 MoneyPass ATMs, international wires, APYs up to 4%, and FDIC insurance up to $3 million.

Fast payments, up to 4.00% Annual Percentage Yield (APY), and up to $3M in FDIC insurance

Best money transfers – Mercury

Mercury sets itself apart by offering low-cost money transfers, including fee-free ACH transfers (0 to 1 days), domestic wires (1 to 3 days), and international wires (1 to 3 days).* If you’re transferring money frequently, this could be your best bet.

*If a currency conversion is involved in an international transfer, a fee will apply.

Best for ATM access: Relay

Relay includes fee-free access to a global network of over 55,000 Allpoint ATMs. Plus, the company doesn’t charge a fee when customers use out-of-network ATMs (although standard third-party fees can still apply).

Best for earning interest: NorthOne

NorthOne offers a 2.50% APY on balances up to $250,000 on its free plan, and an APY ranging from 1.78% to 2.50% for balances exceeding that amount. While Lili offers a higher APY of 4% for balances from $500,000 to $1 million, NorthOne comes out ahead by 0.25% on its APY for accounts holding $250,000 or less.

Best for cash deposits – Found

Found allows you to deposit cash at over 40,000 retail stores nationwide—such as CVS, Family Dollar, and 7-Eleven—for a fee of only $1.75 per deposit. This is lower than the Green Dot fee, which can range up to $4.95 per deposit.

Comparison Table

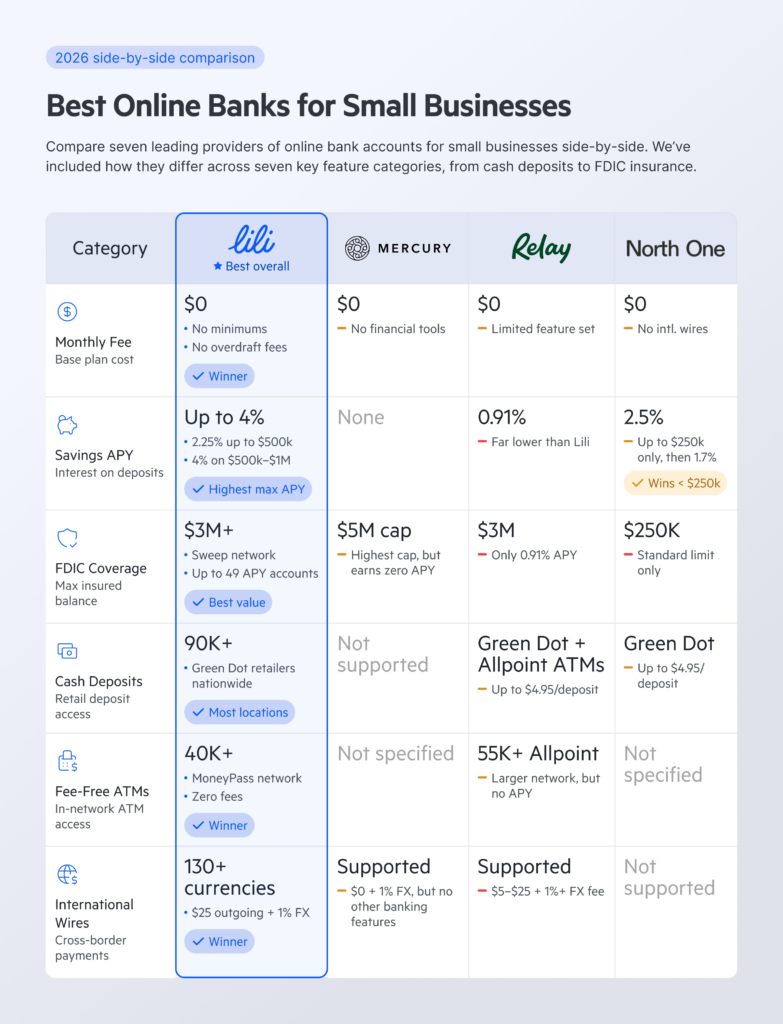

Now, let’s dive a bit deeper. Below, you can compare seven leading providers of online bank accounts for small businesses side-by-side. We’ve included how they differ across seven key feature categories, from cash deposits to FDIC insurance.

| Cash deposit options/fees | ACH fees/speed | Domestic wire fees | International wire fees | APY | FDIC insurance Cap | Best For | |

| Lili | Green Dot retailers (fee up to $4.95) | Standard: Free; Expedited: 1.50% of the transaction amount ($0.50 to $20) | Incoming: $0; Outgoing: $15 | Incoming: $15, Outgoing: $25 + 1% currency conversion fee | 2.25% on up to $500K, 4% on savings balances $500K to $1M | Up to $3M | Growing businesses, teams of up to 10 |

| Relay | Green Dot retailers (fee up to $4.95) and Allpoint ATMs (no fee) | Standard: Free; Expedited: $5 | Incoming: $5; Outgoing: $8 | Incoming: $0; Outgoing: $5 or $25 + 1%+ currency conversion fee | 0.91% | Up to $3M | Businesses working based on the profit-first method |

| Bluevine | Green Dot retailers (fee up to $4.95) and Allpoint ATMs ($1 + 0.5% of deposit amount) | Standard: Free; Expedited: $10 | Incoming: $0, Outgoing: $15 | Incoming: $15; Outgoing: $25 + 1.5% currency conversion fee | 1.3% on balances up to $250K | Up to $3M | Businesses that want built-in accounts payable. |

| Novo | None | Standard: Free; Expedited: 1.5% of transaction ($0.50 to $20) | Incoming: $0; Outgoing: $30 | Incoming: $0; Outgoing: Outsourced to WIse | None | Up to $250K | Freelancers |

| Found | Vanilla DirectPay retailers ($1.75 fee) | Standard: Free; Expedited: 1% of transfer amount ($1 to $25); Instant: 1.75% of transfer ($0.50 minimum) | Incoming: $0; Outgoing: $15 | Not supported | None | Up to $250K | Gig workers and side hustlers |

| Mercury | None | Same-day, next-day: Free | Incoming: $0; Outgoing: $0 | Incoming: $0; Outgoing: $0 + 1%. currency exchange fee | None | Up to $5M | Tech startups |

| NorthOne | Green Dot retailers (fee up to $4.95) | Standard: Free; Expedited: 1.5% of transaction ($1-$20) | Incoming: $0; Outgoing: $20 | Not supported | 2.50% APY balances up to $250K, then 1.78% to 2.50% | Up to $250K | People who want to use the envelope method |

How We Chose (Methodology)

Lili’s list of the best online banks for small businesses is based on in-depth research. We collected the most recent data available from seven leading business banking service providers serving U.S. small business owners. We reviewed each company across 17 feature categories, leading to over 100 data points. Data was sourced from provider product pages, pricing pages, disclosures, and fee schedules.

The Key Factors That Actually Matter

As you review online bank account options for your small business, here are seven key factors to consider:

1. Support: Customer support is important when choosing an online bank account. You want to improve the odds that a company or bank will handle any issues that come up promptly and fairly. Look for providers with multiple support channels, such as a customer service phone line, email support, secure messaging, and live chat. Additionally, check sites like the Better Business Bureau (BBB) and Trustpilot to see if a provider has any notable trends in customer complaints, such as difficulties reaching resolutions or slow responses.

2. Yield: Some business bank accounts pay an annual percentage yield (APY) just for keeping your money in the account. These offers often include a specific APY on bank balances up to a certain amount, or may feature different APYs that apply to different balance ranges. Consider APY offers and how they impact the overall value an account offers your business.

3. Transfer limits and hold times: Online bank account providers vary greatly in the speeds, fees, options, and limits they offer for money transfers. You’ll want to assess your needs for ACH transfers, domestic wire transfers, and international wire transfers upfront. Then, look for a bank account that can support your needs with competitive offerings. Many companies and banks offer free standard ACH transfers, which take one to three business days, and expedited same-day ACH transfers for a small fee. Outgoing domestic wires tend to be more expensive than ACH transfers, while international wires come with even higher wire fees–along with the potential for an additional currency conversion fee.

4. Limits and fees: We’ve mentioned limits and fees in the above sections, but they extend beyond these areas. For example, you’ll want to check limits on FDIC insurance and daily debit card transactions, along with fee amounts for overdrafts, non-sufficient funds, and foreign transactions. It’s important to review the full fee schedules and limit tables of potential providers to understand all of the limits and fees that will apply. These will determine your overall costs as well as whether the account can suit your needs.

5. Tools: The tools an online bank account provider offers alongside its online business banking accounts are also worth considering. Some companies offer a suite of financial services that can help to streamline your financial operations. For example, you may find software to support bill pay, invoicing, accounting, tax preparation, payroll, and building business credit. If you’re looking to consolidate various financial tools into one platform, look for providers with more comprehensive offerings.

6. Cash deposits: Online bank account providers generally allow you to fund checking accounts through various electronic methods, such as ACH transfers, mobile check deposits, transfers from linked accounts, and inbound wires. Cash deposits, on the other hand, aren’t always supported. Being so, if your business receives cash payments that you want to deposit into your bank account, it’s important to check if cash deposits are allowed. When they are, look into the specific costs, limits, and available deposit locations. Many times, online bank providers facilitate cash deposits through deposit partner networks (like Green Dot), which come with a fee per deposit.

Switching Banks Without Breaking Your Business

Once you find the right bank account for your needs, the next task is to sign up and migrate over. While it can be a fairly straightforward process, there are a few important steps to keep in mind.

- First, create an online account.

- From there, take note of your new account’s ACH, debit card, and wiring information, and update it with all third parties you pay or who pay you. This may include everyone from vendors and lenders to utility companies, subscription providers, and the IRS. While the goal is to prevent payments from falling through the cracks, it’s a good idea to keep the old account open for at least 30 to 60 days, just in case.

- Also, be sure to export any statements you need from the old account during this period.

- Next, be sure to link the new account to any third-party programs you’d like to integrate, such as accounting and payroll software.

- And, lastly, set up role-based permissions for anyone who will have access to the account.

Where Lili Fits

Advanced business banking is part of all of our offerings at Lili, including the no monthly fees Lili Core base plan. Lili’s online checking and savings accounts are best for those who want a solid all-around business bank account, especially growing businesses with teams of up to 10. Lili has been rated 4.7 out of 5 stars after receiving over 4,000 reviews on Trustpilot, and was named the best U.S. digital bank for SMBs in 2025 by the International Investor awards.

A few notable features you get with Lili include top-notch customer service, an APY of up to 4%, up to $3M in FDIC insurance, fast payments, various integrations, and team access. You can also make cash deposits at over 90,000 GreenDot retail locations and use over 40,000 MoneyPass ATMs without paying fees. And if you want additional financial tools, you can upgrade your plan to get access to advanced accounting, tax preparation, and credit-building services.

What ‘Online Bank’ Means (Bank vs Fintech)

Many providers of online bank accounts are not actually banks. Instead, they’re financial technology (fintech) companies that extend the banking services of banks to their customers. For example, Lili’s banking services are provided by Sunrise Banks, N.A., Member FDIC. As a result, the Lili Visa Debit Card is issued by Sunrise Banks, pursuant to a license from Visa U.S.A, Inc.

Further, Lili’s FDIC insurance is provided by Sunrise Banks and the Sweep Network, which automatically allocates deposits across multiple FDIC-insured banks to increase coverage up to $3 million. While fintechs aren’t banks, banking services are built right into their platforms, so the user experience is seamless from the customer’s perspective. The average user wouldn’t realize the fintech wasn’t directly providing its banking services if it weren’t for the required disclosures.

FAQ

Learn more about choosing the best online bank as a small business owner.

What is the best online bank for a small business?

The best online bank for a small business depends on the needs and priorities of that particular business. For example, Lili offers a competitive, all-around offering for growing businesses with teams of up to 10 people. Mercury, on the other hand, is best for tech startups while Novo caters to freelancers.

Can I open a business account online with an EIN only?

The requirements to open a business bank account vary from one provider to the next, but you will need more than just an EIN. Common requirements include business formation documents, an operating agreement, an IRS EIN letter, government-issued IDs for the owners, and a utility bill or lease to verify the physical business address.

Are fintech business accounts FDIC-insured?

When bank accounts are offered by fintech companies, the banking services are provided by an FDIC-insured partner bank. As a result, the funds in the bank account are insured by the FDIC, up to the limits provided by the bank.

Do online banks accept cash deposits?

Many online bank accounts allow customers to make cash deposits, but not all. It will vary by provider. When allowed, cash deposits are often accepted through deposit partner networks or ATMs.

What is best for international payments?

Mercury stands out for low-cost, fast international wire transfers. Both incoming and outgoing international wires are low-cost and completed in one to three days. Further, you can send payments to over 40 countries, and the company’s currency exchange fee is just 1%. However, it’s important to weigh all of the features a bank offers to ensure it’s a good fit for your company’s needs overall.

Summary – Get Help Picking the Right One (60-second checklist)

Online banking offerings can vary greatly in terms of features, limits, and costs. The account that offers the best value for your small business will depend on your specific needs and preferences. To help you find the right fit, here’s a quick list of questions, along with bank account providers that can be a good fit based on your answers.

Step 1: How do you handle money day-to-day?

- Cash-heavy business? → Lili, Relay, Bluevine, Found, NorthOne

- Electronic? → Any, keep going

Step 2: How fast do you move money?

- Is same-day ACH needed often? → Lili, Novo, Found, Mercury

- Do you need expedited check deposits? Lili

- Frequent international wires? → Lili, Relay, Bluevine, Found, Novo, Mercury

Step 3: How much do you keep in the account?

- Does earning interest matter? → Lili, NorthOne, Bluevine

- Balances over $250K? → Lili, Relay, Bluevine, Mercury (Sweep Networks)