Looking to open a U.S. business bank account from abroad? Here are 3 top options for non-resident founders.

Once you establish a U.S. business as a non-resident, opening a bank account in the U.S. is a natural next step. While cross-border transfers are sometimes necessary for businesses, they can quickly become expensive and slow operations when used as the default. A U.S. bank account allows for faster, lower-cost domestic transfers, along with cleaner accounting, easier integration with U.S. payment processors, and expanded access to U.S. financial services. However, you may run into a few obstacles when you attempt to open one. Read on to learn what to expect—plus find our picks for the three top U.S. business bank account providers for non-residents.

Can you open a U.S. bank account online as a non-resident?

It’s possible to open a U.S. bank account online as a non-resident, but your ability to do so will vary from one financial institution to the next. In many cases, traditional banks require you to schedule an in-person appointment and physically visit a bank branch to complete the account establishment process. On the other hand, some of the more digital-forward financial service companies, like Lili, allow you to open an account entirely online.

What do non-residents usually need to open a U.S. business bank account?

To open a U.S. bank account, non-residents typically need to meet various eligibility requirements, submit the required documentation, and get approved. Common requirements include:

- Identification documents: Beneficiary owners of the business need one to two forms of government-issued identification, often a foreign passport and a foreign driver’s license.

- Beneficial owner information: Non-resident beneficial owners often must provide the source of income they used to start the business, share whether the business is new or established, report their annual personal income, and note the countries in which the business operates.

- EIN: The business must have an Employer Identification (EIN) from the IRS and present its CP-575 EIN Confirmation Letter.

- Entity documents: Organizations often require the submission of entity formation documents, such as the company’s operating agreement, articles of incorporation, certificate of formation, or corporate bylaws.

- Proof of address: Proof of address is often required, business and/or personal. Acceptable documents may include a utility bill, a signed lease agreement, a pay stub from the latest period, tax documents from the recent year, a bank statement, or an insurance bill or statement.

- Appointment: In some cases, providers require applicants to deliver their documents in person at a brick-and-mortar branch. In others, the submission can be done remotely online.

While these are common requirements for non-residents, the specifics will vary by bank account provider. It’s important to check the requirements of any provider you’re considering.

3 main paths to business bank accounts

Non-residents can opt for a few different paths to opening a U.S. bank account, including opening the account with the following three types of institutions.

Traditional banks

Many traditional brick-and-mortar banks, such as Bank of America and Wells Fargo, allow non-citizens and non-residents to open U.S.-based business bank accounts. These institutions often require applicants to schedule an appointment in a physical branch and set up the account in person.

Pros:

- Established, reputable institutions

- Physical branches for in-person support

- FDIC insured

Cons:

- Often requires an in-person visit

- Higher fees are common

- Slower onboarding process

Best for: Non-resident founders who plan to spend time in the U.S., want in-person support, and prefer working with a well-established traditional bank.

Online-first options

Online-first providers of business bank accounts, such as Lili and Mercury, primarily offer banking services online. They tend to have lower fees and offer higher interest yields than traditional banks due to their reduced overhead. Further, non-residents can often open accounts remotely, saving them a trip to the U.S.

Pros:

- Fully remote account opening (in many cases)

- Lower fees

- Faster application process

- FDIC insured

Cons:

- No physical branches

- Eligibility restrictions based on country of residence

Best for: Digital-first small businesses, startups, and founders who want a straightforward, low-cost business bank account they can open from abroad.

Global money-service businesses

Global money service businesses are non-bank financial institutions that allow entities to open accounts, hold balances, and make transfers. Examples include PayPal and Wise. These can be preferable for companies that need to hold multiple currencies or perform regular cross-border transfers. They typically offer competitive foreign exchange rates and lower international transfer fees compared to traditional banks.

Pros:

- Multi-currency accounts

- Competitive FX rates

- Lower international transfer fees

- Easy international payments

Cons:

- Not full-service banks

- Limited access to credit products

- Funds may not be directly FDIC-insured (depends on structure)

- May have account freezes or compliance reviews

Best for: Businesses that operate globally, handle multiple currencies, or frequently send and receive international payments.

Top 3 online business banking options for non-residents

The following three online business banking providers offer competitive banking products for non-residents, along with streamlined digital application flows.

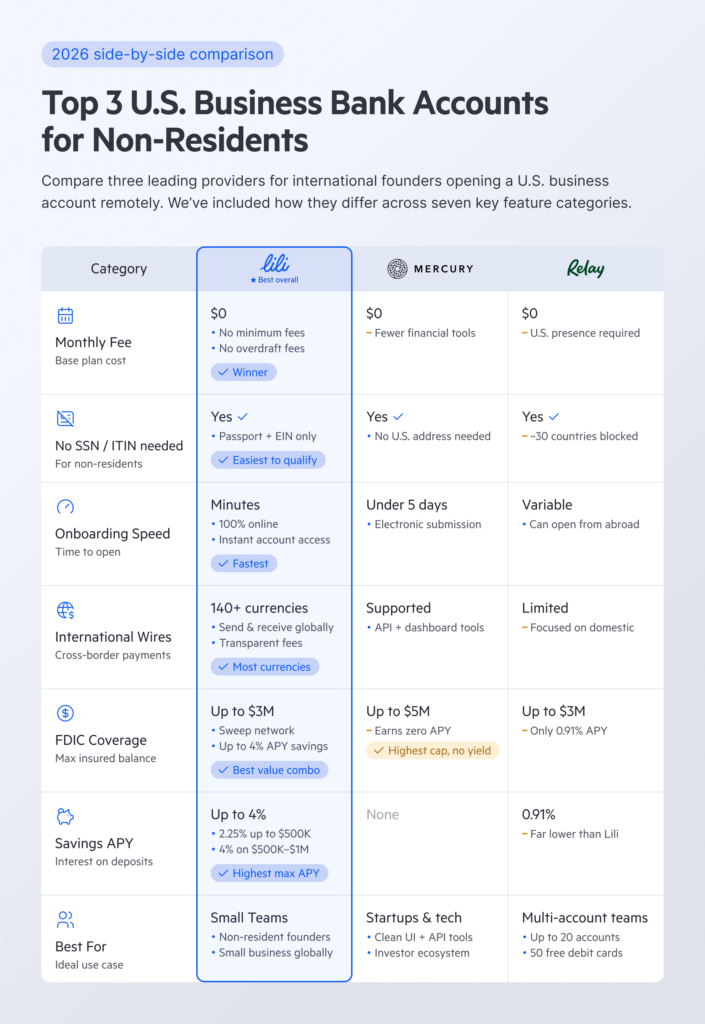

Lili: Best for small teams

Monthly fee: $0 for Lili Core

APY: Up to 4.00% on savings accounts

FDIC Insurance: Up to $3 million

Lili offers online business bank accounts to non-U.S. citizens living outside the U.S. in over two dozen countries, as well as to non-resident aliens living in the U.S. Accounts can be opened remotely without an in-person U.S. trip.

Key perks:

- Fast domestic payments: You can move funds fast with Express ACH, expedited check deposits, and domestic wires. Plus, you’ll receive early ACH access, where funds can post to your account up to two days before scheduled payment dates.

- International wires: Lili supports inbound and outbound international wire transfers for 130 global currencies and over 50 countries— with no FX fees.

- Customer support: You can reach a real support specialist five days per week by phone and seven days per week by email. Plus, an AI assistant is available 24/7.

- No U.S. physical address requirement: You don’t need a physical address in the U.S. to open an account with Lili. However, you will need a U.S. mailing address to receive your Lili Visa Debit card.

To qualify, you’ll need to have citizenship in a supported country, a registered business in the U.S., and an EIN. From there, you can send over all the necessary documentation electronically and complete the application process online.

Mercury: Best for tech or SaaS companies

Monthly fee: $0 for Mercury

APY: None on standard checking or saving accounts

FDIC Insurance: Up to $5 million

Mercury is another provider of online business bank accounts, but it caters to startups, e-commerce companies, and tech companies. To be eligible for a Mercury account, you don’t need to live in the U.S. or be a U.S. citizen. Founders can be from any country, excluding the 50 featured on Mercury’s prohibited country list. Unlike Lili, however, your business will need a physical address in the U.S. and a PO box won’t suffice.

Key perks:

- API access: Mercury offers API access for those who want to build custom workflows.

- Free wires: No fees are charged on domestic or international USD wire transfers.

- Advanced rules: You can create extensive user-level permissions and controls.

The onboarding process with Mercury involves submitting information about the company’s beneficial owners and submitting all the documentation electronically.

Relay: Best for Profit-First Method

Monthly Cost: $0 for Relay Starter

APY: 0.91% on savings accounts

FDIC Insurance: Up to $3 million

Relay is another option to consider for international founders. You don’t have to be a U.S. citizen or resident to qualify and can open the account from abroad—as long as your country isn’t on Relay’s prohibited list of about 30 countries.

Key perks:

- Extensive account structure: Create up to 20 individual checking accounts to separate funds for expenses, profit, and taxes.

- Cash back on spending: Earn up to 1.5% cash back on credit card spending.

- Team debit cards: Get up to 50 free Visa debit cards per business, which can include virtual or physical debit cards.

To qualify, your business must have a U.S. operating presence and a physical U.S. address. Note, a Registered Agent address won’t work. Beyond that, you’ll also be able to submit all the required documentation electronically.

Step-by-step checklist to improve approval odds

To improve the odds of getting approved for a U.S. bank account as a non-resident, keep these steps in mind:

- Form a U.S. entity: Before trying to apply for a business bank account, you need to form a legal entity in the U.S. by registering your business as an LLC or corporation at the state level.

- Secure Your EIN: Request an EIN from the IRS before you apply and save the CP-575 confirmation letter.

- Confirm country eligibility: Review the provider’s prohibited or restricted country list and ensure your home country is eligible before applying.

- Verify address requirements: Check what type of business addresses the provider requires. It can vary between a physical U.S. address, a U.S. mailing address, or a foreign address. Further, additional restrictions may apply regarding PO boxes and registered agent addresses.

- Check for in-person requirements: Check whether you need to visit a bank branch in person to complete the application process. If you have a preference, find a bank that meets your needs.

- Prepare government identification: Ensure you have clear digital copies of eligible government-issued identification documents for all beneficial owners.

- Gather documentation: Review the bank account provider’s documentation requirements and ensure you have everything you need. Double-check all of the documents to ensure the information is complete and accurate.

- Shop around: Shop around to find a shortlist of bank account providers that offer competitive costs, the services you need, and look like a good fit, eligibility-wise.

Fees to watch

Along with finding a U.S. bank account that aligns with your needs, the account needs to fit your budget. Be sure to review the fee schedules of the bank accounts you’re considering to see how much they’ll cost you. Common fees to note include monthly service fees, ATM fees, wire transfer fees, expedited ACH fees, and overdraft fees. If you choose an account with expensive fees on services you’ll use often, it can eat into your bottom line unnecessarily.

Find the right business bank account for your needs

As a non-resident founder, you may encounter a few obstacles when shopping for a U.S. business bank account.

Some providers simply don’t serve non-residents, and instead require founders to have a Social Security number or ITIN for identity verification. Others will approve non-residents, but require your business to have a U.S. physical address. Further, you may encounter providers that don’t serve founders who live in your country, or that require you to visit a branch in the U.S. to open the account.

However, don’t get discouraged if you encounter a few bank account providers that won’t work for your specific situation. Each has different rules and requirements, and some are much more flexible than others. For example, Lili allows you to open an account remotely, doesn’t require a physical U.S. address for your business, and has low fees.

The shortlist of three top bank accounts for non-residents can jumpstart your journey of shopping around to find a competitive business banking option. Learn more about Lili’s business banking for non-residents!