Building business credit is a sequential process that starts with your business structure and ends with an active, monitored credit profile across all three major business credit bureaus. This guide covers every step in order — because skipping any one of them will slow down or block the steps that follow. Whether you’re launching an LLC from scratch or formalizing a business that’s been running on personal credit, the roadmap below gives you exactly what to do and why the sequence matters.

To build business credit, you need to register a legal business entity, obtain an Employer Identification Number (EIN) from the IRS, open a dedicated business bank account, register with business credit bureaus, establish vendor and trade credit through net-30 accounts, apply for a business credit card, and monitor your reports across Dun & Bradstreet, Experian Business, and Equifax Business. Each step builds on the previous one — none can be skipped without consequences downstream.

🎧 On the go? Listen to our podcast episode, “Mastering Business Credit,” for a clear, actionable breakdown of how to establish and grow your business credit from day one.

What is business credit and why does it matter?

Business credit is a financial profile tied to your business entity — not to you personally. It records how your company pays its bills, manages debt, and handles credit obligations, and it is used by lenders, vendors, suppliers, and insurers to evaluate your business as a borrower or partner.

The separation between business credit and personal credit is not just administrative. A strong business credit profile lets you access financing and lines of credit under your company’s name, with your company’s payment history as the qualifying factor — not your personal credit score. That separation protects your personal assets if the business runs into financial difficulty.

Beyond protection, business credit is a practical growth tool. Companies with established profiles qualify for higher credit limits, better interest rates, and favorable vendor payment terms — such as net-30 or net-60 windows — that improve working capital and cash flow. Vendors and suppliers treat a business with a solid credit profile as more stable and worth extending terms to. If you plan to scale, building that profile is not optional.

How does business credit scores work?

Business credit is scored by three separate bureaus, each using its own model and scale. Unlike personal credit scores — which are private — business credit scores are generally available to the public. Any vendor, lender, or prospective partner can check your business credit score before deciding to work with you.

| Bureau | Score Name | Score Range | What It Measures | Cost to Monitor |

| Dun & Bradstreet | PAYDEX | 0–100 | Payment promptness | Free basic / paid detailed |

| Experian Business | Intelliscore Plus | 1–100 | Payment risk | Free basic / paid detailed |

| Equifax Business | Business Credit Risk Score | 101–992 | Delinquency likelihood | Free basic / paid detailed |

Dun & Bradstreet (PAYDEX)

The PAYDEX score, issued by Dun & Bradstreet (D&B), runs from 0 to 100 and measures how promptly your business pays its financial obligations. A score of 80 or above indicates consistent on-time payment and is widely considered the threshold for a “good” business credit score with D&B. A score of 100 — reflecting consistently early payment — is the highest achievable and signals to suppliers and lenders that your business is a reliable payer.

Experian Business

Experian Business issues the Intelliscore Plus, which also runs on a 1–100 scale and assesses payment risk — specifically, the likelihood that your business will become seriously delinquent within the next 12 months. A score of 76 or above places your business in the low-risk tier. Experian Business draws on trade payment history, public records, collections data, and business demographics to generate the score.

Equifax Business

Equifax Business uses the Business Credit Risk Score, which ranges from 101 to 992. This score measures the probability that your business will incur a severe delinquency within the next 12 months. Higher scores indicate lower risk. Equifax Business also produces secondary scores — including a payment index and a business failure score — which some lenders evaluate alongside the primary risk score.

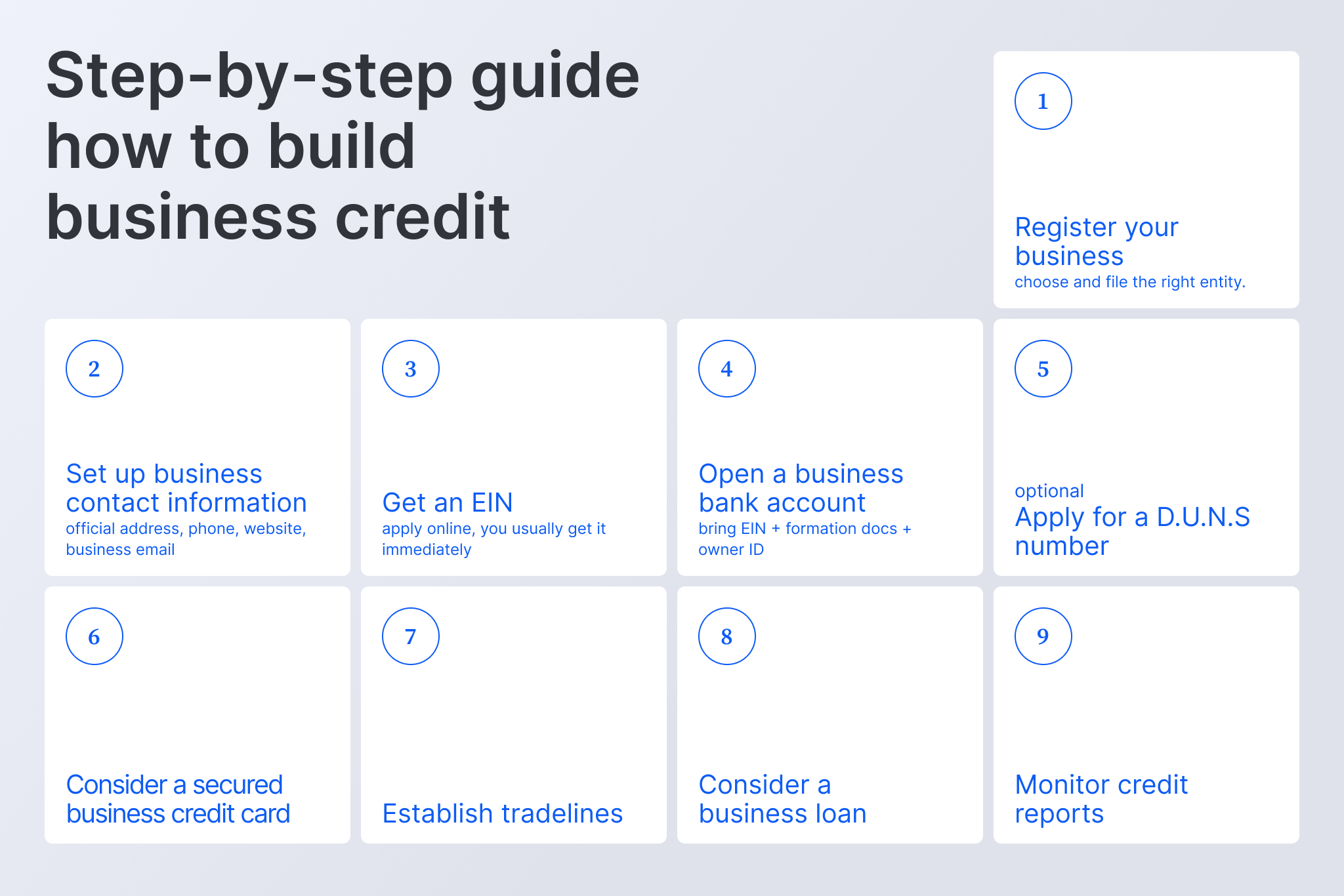

How to build business credit (step by step)

1. Register your business as a legal entity

Forming a legal entity is the prerequisite for every step that follows — without it, you have no separate business identity that bureaus or lenders can track. Before any credit account can be separated from your personal finances, your business must exist as a distinct legal structure.

The two most common formations for small business owners are the limited liability company (LLC) and the corporation. Both create a legal separation between you and your business, which means creditors pursuing unpaid business debts cannot automatically attach your personal assets. A sole proprietorship does not provide that separation — the owner and business are treated as one legal and financial entity, which makes building a standalone business credit profile nearly impossible.

To register, file the appropriate formation documents with your state’s Secretary of State office. You will choose a business name, pay a state filing fee, and in most states complete the process online. Once registered, your business has its own legal identity — and that identity is what all future credit accounts, EIN applications, and bureau profiles are built around.

2. Get your Employer Identification Number (EIN)

An Employer Identification Number (EIN) is the federal tax identification number assigned to your business by the Internal Revenue Service (IRS). It functions as a Social Security number for your business — a unique nine-digit identifier that connects all of your business’s financial activity in the eyes of lenders, credit bureaus, and government agencies.

You need an EIN to open a business bank account, apply for business credit accounts, and register your profile with D&B, Experian Business, and Equifax Business. Without it, any credit activity will be tied to your personal Social Security number — which defeats the purpose of building separate business credit.

Applying for an EIN is free and takes minutes at irs.gov. The online application returns your EIN immediately upon submission. Do not pay any third-party service to obtain one — numerous websites charge fees for a process the IRS provides at no cost. Apply the same day you complete your entity registration.

3. Open a business bank account

A dedicated business bank account is the first visible evidence that your business operates as a financially separate entity — and lenders treat it as such. When you apply for a business loan or line of credit, the lender will typically request business bank statements alongside your credit report. A bank account that shows consistent deposits, managed cash flow, and responsible spending builds a banking history that directly supports your future credit applications.

Your business checking account must be opened in your company’s legal name using your EIN. Every business expense — vendor payments, software subscriptions, payroll, operating costs — should flow through that account exclusively. Mixing personal and business transactions in the same account is one of the most common and costly mistakes early-stage business owners make; it blurs your credit profile and complicates tax reporting.

When selecting a business bank account, look for low or no monthly fees, online bill pay, and a clear path to additional products like a business credit card or line of credit. Your relationship with a bank often carries weight when those credit applications come later. Open a business bank account today — it becomes the financial foundation that every subsequent step in this process depends on.

4. Register with business credit bureaus

Most bureau profiles begin populating automatically once lenders and vendors report your payment activity — but Dun & Bradstreet requires proactive registration, and getting that done early is one of the highest-leverage actions you can take to establish business credit.

How to Get a D-U-N-S Number

A D-U-N-S number (Data Universal Numbering System number) is a unique nine-digit identifier assigned by Dun & Bradstreet to your business. It is how D&B tracks your credit activity and what lenders use to pull your PAYDEX score. Without a D-U-N-S number, your business has no profile with D&B — the largest and most widely referenced business credit bureau in the United States.

Apply for your D-U-N-S number for free at dnb.com. Standard processing takes up to 30 business days; an expedited option is available for a fee if faster setup is required. Once issued, your D-U-N-S number stays with your business permanently. Register as soon as your entity is formed and your EIN is secured — every week without an active D&B profile is a week of potential PAYDEX history that cannot be recovered.

Experian Business and Equifax Business will begin building your profile automatically as creditors and vendors report your payment behavior. Both bureaus have business portals where you can monitor your profile and check for inaccuracies as your history develops.

5. Establish vendor and trade credit

Vendor and trade credit — structured as net-30 accounts — are the most accessible entry point for building business credit when you have no established credit history. A net-30 account means a supplier extends you up to 30 days to pay for goods or services after delivery, and then reports your payment behavior to one or more of the business credit bureaus.

This is where many businesses lose significant ground: they open accounts with vendors who extend credit but do not report to the bureaus. If the vendor doesn’t report, the account produces no credit history regardless of how reliably you pay. Before opening any vendor credit account, confirm that the supplier reports to at least one of the three major bureaus — D&B, Experian Business, or Equifax Business — and that they report monthly, not quarterly.

The PAYDEX score rewards early payment specifically, not just on-time payment. A business that pays before the due date consistently will score higher than one that pays exactly on the due date. For businesses starting from scratch, opening three to five net-30 vendor accounts — all with confirmed reporting vendors — and paying each invoice before it’s due is the most reliable way to build an active D&B profile and move your PAYDEX score quickly toward the 80-plus range.

6. Apply for a business credit card

A business credit card is one of the most effective instruments for building a business credit profile, provided it reports to the business credit bureaus rather than only to personal credit bureaus. That distinction matters before you apply — not all business credit cards report business activity to D&B, Experian Business, or Equifax Business.

Look specifically for a card that reports to the major business bureaus. Some cards report to all three; others report only to personal bureaus under the cardholder’s Social Security number, which does nothing for your business credit profile. If separating your business credit entirely from your personal finances is a priority, corporate card products that issue on the basis of your EIN with no personal guarantee are available to qualifying businesses — these report to business bureaus and are evaluated on your business’s financial standing rather than your personal credit score.

Once you have a card, keep credit utilization below 30% of your available credit limit and pay the balance in full each month wherever possible. High utilization and missed or late payments are the two fastest ways to damage a business credit score. Treat the card as a payment tool — use it for regular business expenses you would pay anyway, then pay it early. That pattern, consistently maintained, builds a strong payment history with each bureau that receives the reporting.

7. Monitor your business credit reports

Monitoring your business credit reports is an ongoing responsibility — not a one-time setup task. Errors appear on business credit reports more often than most owners expect, and because business scores are public, an inaccurate report can quietly cost you vendor terms or loan approvals before you are aware of the problem.

Check your reports with all three bureaus — Dun & Bradstreet, Experian Business, and Equifax Business — at least three to four times per year. Each bureau holds different information about your business, and an error with one does not automatically appear on the others. Monitoring tools range from free basic access through each bureau’s own portal to paid services that aggregate all three reports in a single dashboard. Detailed reports with full score breakdowns typically cost $50 to $200 per bureau annually.

When you find an error — a payment marked late that was made on time, a vendor account that isn’t appearing, or an unrecognized inquiry — dispute it directly with the relevant bureau using their formal dispute process. Errors that go unchallenged stay on your profile indefinitely. Prompt correction ensures your business credit score reflects your actual payment behavior.

How long does it take to build business credit?

Building business credit is measured in months, not days, and there is no shortcut that changes that reality. With the right steps in sequence — a registered entity, an active EIN, a business bank account, and at least three reporting vendor accounts — a foundational business credit profile can be established within 30 to 90 days. At that point, your D-U-N-S number is active, initial trade lines are reporting to the bureaus, and your PAYDEX score has begun to form.

A credit profile strong enough to qualify for meaningful business loans, unsecured lines of credit, or high-limit business credit cards typically requires 12 to 24 months of consistent, positive payment history across multiple accounts. Traditional bank lenders generally want to see at least two years of business banking history alongside bureau scores before approving unsecured financing. Alternative lenders may move faster, but the underlying principle is the same: sustained, demonstrable payment behavior builds the score, and no amount of setup speed replaces it.

The steps in this guide are ordered the way they are because the sequence is not arbitrary — each one creates the infrastructure the next step requires. Completing them in order and maintaining discipline from day one is the only reliable path to a lendable business credit profile.

Common mistakes that slow down business credit building

The most damaging mistake is continuing to mix personal and business finances after entity formation. Once you have an LLC or corporation, every transaction must run through your business accounts. Co-mingling funds blurs the boundary between personal and business credit, makes bureau profiles harder to develop, and gives lenders reason to evaluate your business as an extension of your personal financial history rather than a separate entity.

The second most common error is working with vendors who don’t report to the bureaus. Consistent early payment with a non-reporting vendor produces zero credit history. Every net-30 account you open should be verified as a reporting account — with a specific bureau named — before you commit to it.

Delaying the D-U-N-S number application is a third mistake with compounding consequences. Every week without an active Dun & Bradstreet profile is a week of potential PAYDEX history permanently lost. Apply for your D-U-N-S number the same week you register your business entity — there is no reason to wait.

Finally, neglecting ongoing monitoring allows errors, outdated accounts, and occasional fraudulent activity to sit on your reports unchallenged. Business credit reports do not self-correct. If a vendor misreports a payment or an unknown account appears, it will remain on your profile until you dispute it directly with the bureau.