Fill in some basic personal information.

Tell us about yourself

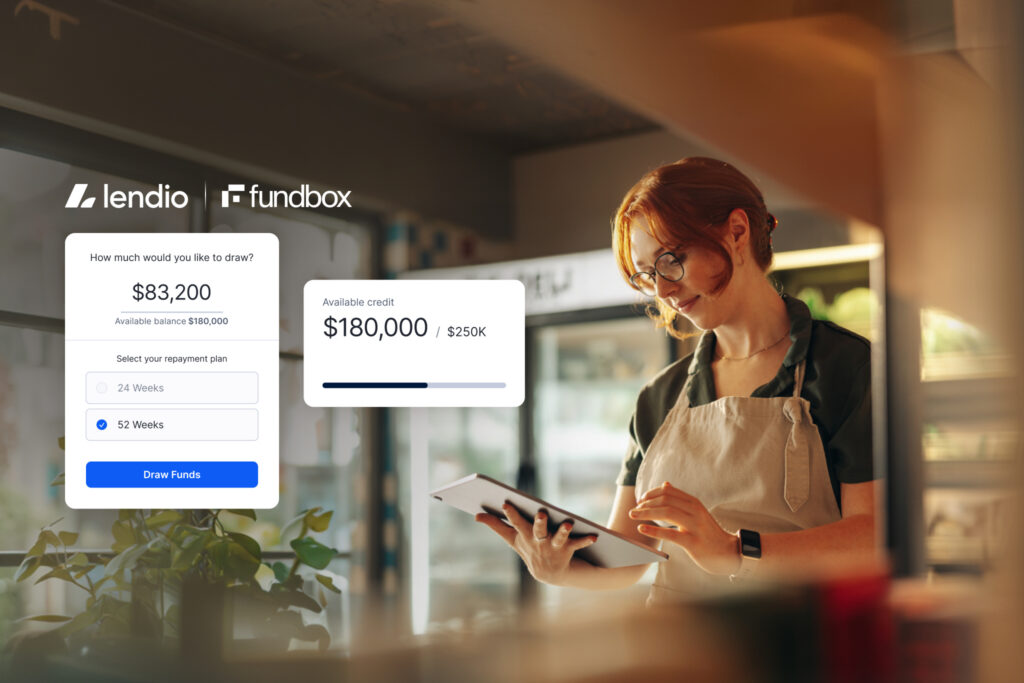

Apply in minutes, fast decisions without impact to business credit score *, and seamless access directly inside the Lili platform: New integrated financing offering expands access to capital through partner-powered options inside Lili

Live support, 7 days a week

[email protected]

(855) 545-4380

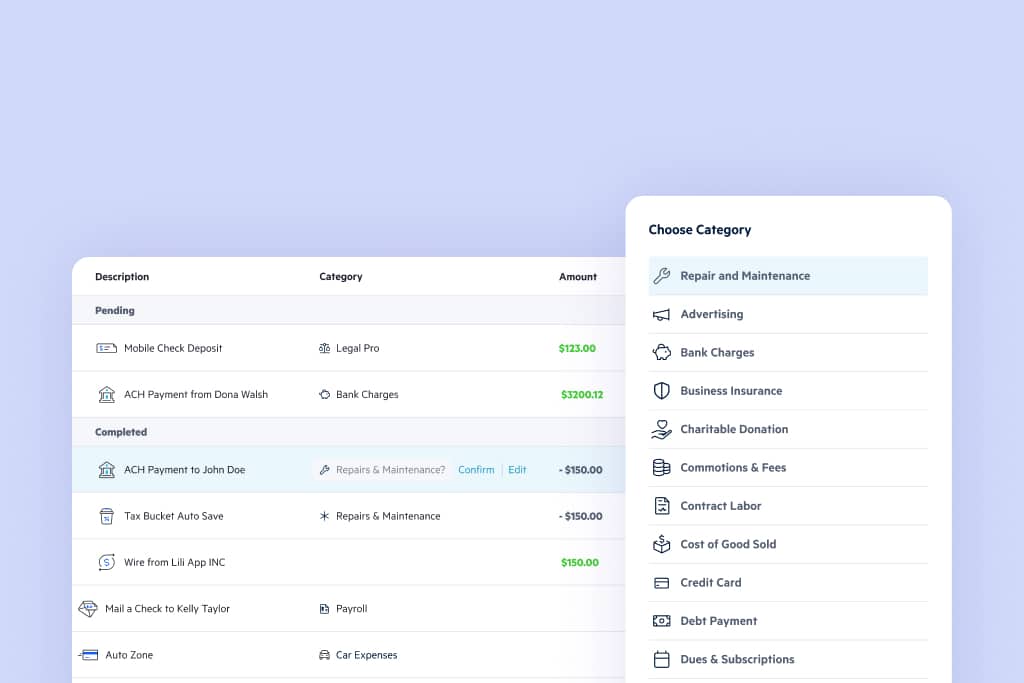

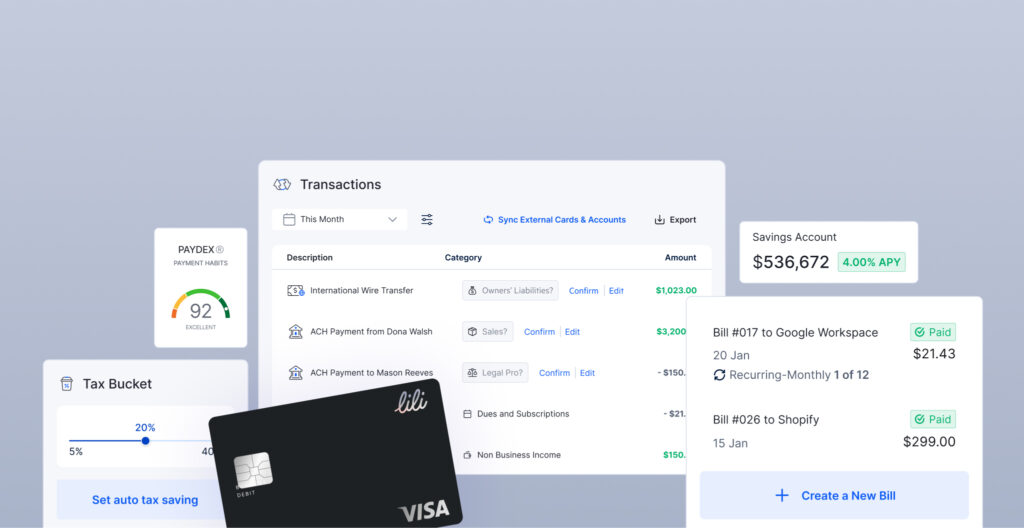

Take a quick tour of the tools inside the Lili account. Banking, bookkeeping, invoicing, and taxes, all in one place.